Jackson Hole

- Stephen H Akin

- Aug 23, 2022

- 6 min read

Updated: Feb 14, 2024

Each year in late August the Federal Reserve Bank of Kansas City hosts dozens of central

bankers, policymakers, academics and economists from around the world at its annual economic policy symposium.

The 2022 Economic Policy Symposium, "Reassessing Constraints on the Economy and Policy," will be held August 25-27. Read more about the symposium's history, which spans more than four decades.

The search is on for a new Kansas City Fed President as Esther L. George has announced that she will be retiring in January 2023.

Ester George is president and chief executive officer of the Federal Reserve Bank of Kansas City.

Read her latest speech, PDF"Looking Back: A 40-Year Perspective on Community Banking".

"Reassessing Constraints on the Economy and Policy,"

Powell Will Face a Tough Audience in Jackson Hole

Analysis by Bill Dudley | Bloomberg

Nearly a year ago, when US Federal Reserve Chair Jerome Powell delivered his speech at the annual economic conference in Jackson Hole, a global audience was hanging on every word for insights into the outlook for growth, inflation and monetary policy in an extremely uncertain environment.

Given how mistaken his assessment proved to be, he’ll have a harder time sounding convincing when he gives his next speech in the same venue later this month. But for the sake of the Fed’s efforts to contain inflation, he’ll have to try.

In his 2021 address, Powell got it wrong in several important ways. He asserted that a transient surge in inflation was “likely to prove temporary,” that the low unemployment rate “understates the amount of labor market slack,” and that “we see little evidence of wage increases that might threaten excessive inflation.” He endorsed the more inflation-tolerant monetary policy framework that the Fed adopted in 2020 as “well-suited to address today’s challenges.”

Powell surely hopes this year’s speech will prove more prescient. I expect him to emphasize three themes: that the economy still has forward momentum with an extremely tight labor market and unacceptably high inflation, that the Fed must tighten monetary policy further to restrain the economy and ease pressure on the labor market, and that the Fed won’t relent until it’s sure it has done enough for long enough to achieve its 2% inflation target.

In delivering this message, Powell must take care to disabuse markets of the notion that the Fed will soon be done tightening monetary policy. Many investors appear to have reached this conclusion based in part on Powell’s statement in July that future interest-rate increases will be data-dependent, ignoring his repeated reference to the Federal Open Market Committee’s interest rate projections indicating a peak considerably above what financial markets expected. The result has been a rally in stocks and bonds that is undermining the Fed’s inflation-fighting efforts.

Powell must make clear that even if the Fed pivots to smaller interest-rate increases in coming months, that does not necessarily indicate a lower peak. As the Fed closes the gap between where monetary policy was and where it needs to be, it may be able to move in a more measured way toward the same ultimate goal. From 2004 to 2006, for example, the central bank brought its interest-rate target from 1% to 5.25% in 17 consecutive 25-basis-point steps. The pace of tightening had little to do with where interest rates peaked.

To convince markets of the Fed’s resolve, Powell will have to be forceful. Many see his warning as mere rhetoric, designed to keep inflation expectations down. They think that once the economy slows, unemployment rises and inflation falls, the Fed will start cutting interest rates long before the 2% target has been achieved. Powell will need to find a way to persuade them that he has no intention of behaving like Arthur Burns (the Fed chair who relented prematurely in the 1970s), lest he later be forced to act like Paul Volcker — who had to correct Burns’s mistake by putting the economy through two recessions.

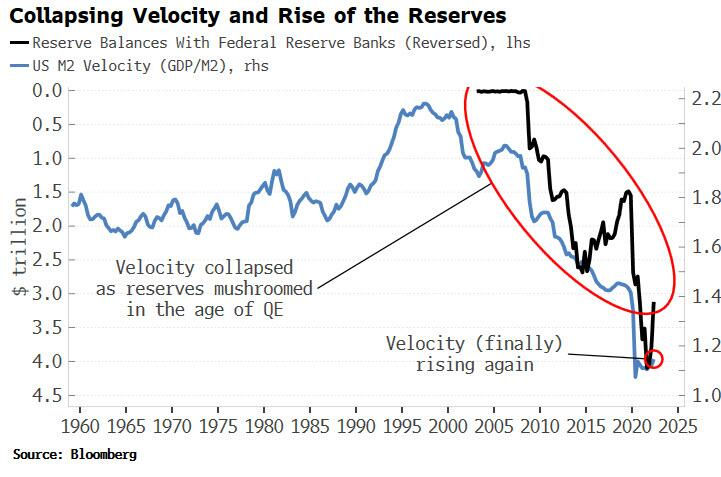

Velocity is Back!

After years of trying to arrest the fall in the velocity of money, it is finally on the rise again.

Velocity is little talked about these days, but in the first throes of the financial crisis it was the center of attention. Defined here as the ratio of GDP to M2 money, velocity continued to fall no matter what the Fed threw at it in the fevered months and years after the Global Financial Crisis:

That’s a major problem when you’re trying to resuscitate demand. Velocity is in essence the average number of times each dollar is spent in the economy, so its inexorable decline meant that, despite the Fed creating trillions of new dollars, total demand was still falling as each dollar was being spent fewer times.

The problem was not causal. Demand was collapsing as households and businesses were in the midst of a major retrenchment in the aftermath of the financial crisis.

Risk appetite was rock-bottom and the main providers of credit to the economy -- banks -- were pulling back from lending in order to rebuild their balance sheets, or just stay alive. The Fed was running up the down escalator as it created ever more reserves only for them to be hoarded by banks, firms and households.

That’s why the Fed was unable to create sustainable inflation despite expanding its balance sheet to unprecedented levels. But the times they are a-changing.

Velocity is related to rates, and falling rates through much of the 2010s meant it fell too. But now that rates are rising, there is a greater incentive for savers to decrease money balances and hold higher-yielding assets, which means a higher velocity of money.

Velocity today is rising faster than it has done since 2010 and is set to keep advancing

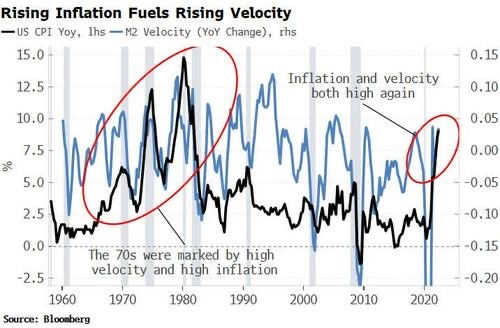

This explains why inflation -- even though it is very likely to fall in the coming months -- will remain persistently elevated above its long-term average and continue to be susceptible to flaring even higher later in the cycle.

Elevated inflation is the spark that lights the fire, and velocity is what fuels it. Rising velocity without high inflation is not normally a problem, but when inflation also starts rising it creates more demand for money and thus velocity rises, with a feedback loop developing. We are on the cusp of that today.

We can now see how the trillions of dollars of hitherto largely idle reserves at the Fed could rapidly become very inflationary. Prices rise, requiring more money to pay for the rising nominal cost of goods and services. Ultimately this means greater demand for reserves, i.e. the velocity of reserves increases, which soon translates into a rise in the velocity of broader money measures too. More inflation ensues.

Even people without much money are experiencing an inflationary-driven increase in demand for it, which is manifesting itself through a rise in bank loans. Rising velocity typically precedes accelerating growth in commercial and industrial loans by about three quarters (C&I loans are a good proxy for loans overall given the stringent lending standards generally attached to them).

Demand for C&I loans is also rising, but banks are tightening their standards for such loans. This is unusual as demand for loans normally falls when standards are being tightened, suggesting demand for loans -- to cover inflation-driven rises in costs -- is overwhelming the tighter loan standards.

More loans means more money, which banks can conjure out of thin air, meaning yet more inflation potential. QT is an attempt to mitigate the inflationary potential of Fed reserves by curtailing velocity. The reduction in reserves should lead to an even greater fall in demand, meaning velocity should fall.

Rate increases, on the other hand, are supposed to work on the demand channel as they can only affect the price of reserves while leaving the volume unchanged.

QE was supposed to work in reverse to QT, causing velocity to rise as demand increased more than the increase in money. We know it failed to achieve that aim. If something fails one way, it’s prudent to assume it might not work in the opposite direction either. Rising velocity will keep the inflation embers alive for some time yet.

TRIPLE PLAY:

Negro Leagues Baseball Commemorative Coins

In July 2019, Missouri Congressman Emanuel Cleaver II introduced the Negro Leagues Baseball Centennial Commemorative Coin Act to the House of Representatives. The Act directed that the U.S. Mint would produce a limited run of three commemorative coins in celebration of the 100th anniversary of the Negro Leagues. Proceeds from the sale of the coins would be given to the Negro Leagues Baseball Museum in Kansas City, Missouri. The Act gained bipartisan approval in the House and the Senate and was signed into law by the President in December 2020.

Connecting America Through Coins

The Commemorative Coin Program The U.S. Mint produces all coinage for the nation. Each year, Congress authorizes that a maximum of two commemorative coin sets be produced to celebrate and honor American people, places, events and institutions.

Since the beginning of the modern commemorative coin program in 1982, the U.S. Mint has raised more than $522 million in surcharges to build or enhance new museums, preserve historic locations and support important national programs. The surcharges are added onto the price of the coin and are turned over to the recipient. The commemorative coins will help “secure a long-term future for this great museum,” according to Bob Kendrick, President of the Negro Leagues Baseball Museum.

Comments